Exploring whether paying one million dollars for the opportunity to live in the United States is a smart investment, weighing benefits, risks, fairness, and long-term impact on immigration policy debate.

A Million-Dollar Path to Life in the United States—Worth It?

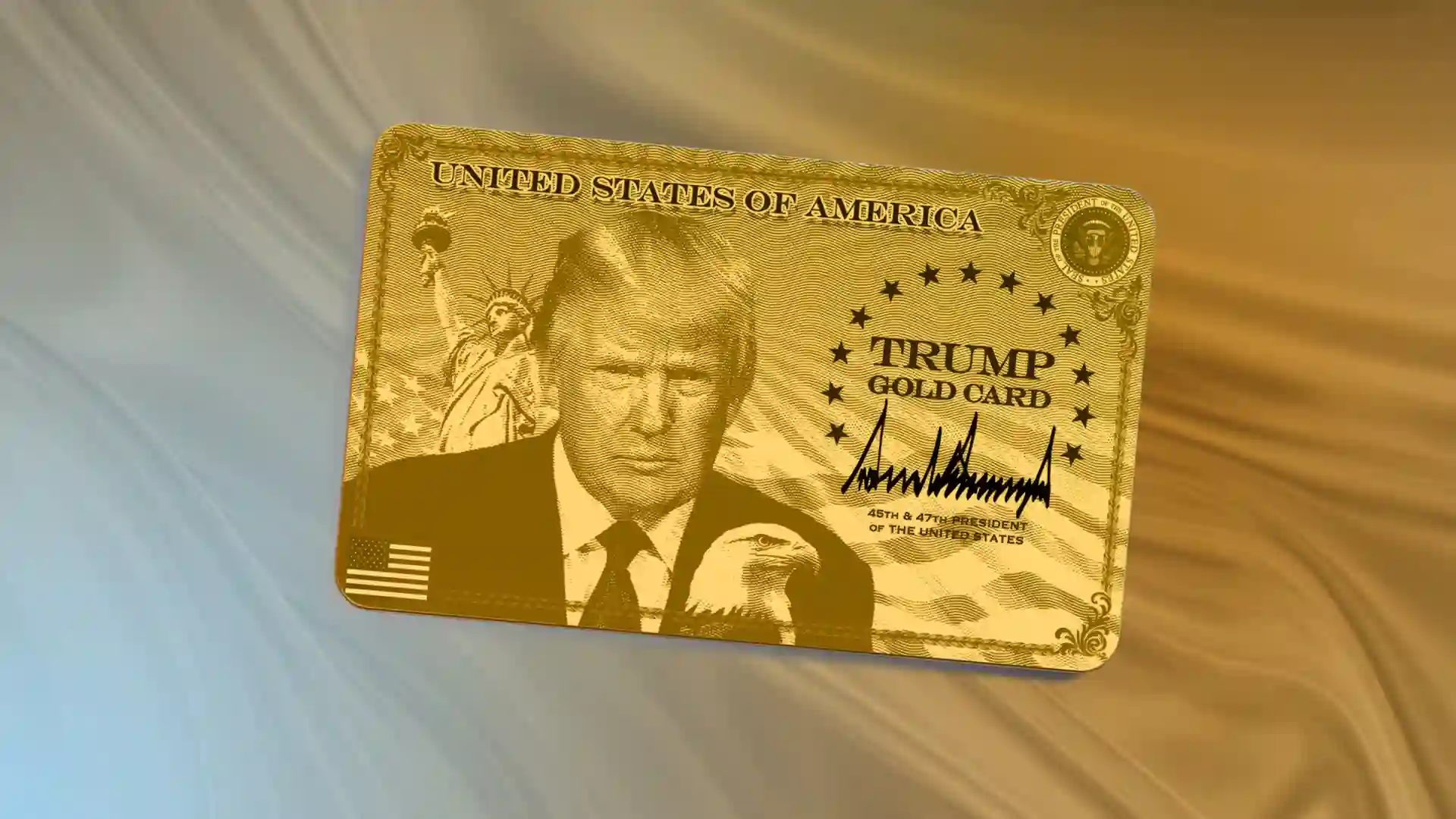

The recently unveiled “Trump Gold Card” visa initiative, introduced by the US President, has sparked strong interest among high-net-worth individuals worldwide. According to Insider18, families and senior business figures across the region view the programme as a major shift in US immigration policy, as it offers a clear and structured path to permanent US residency—without relying on the unpredictability of visa lotteries or traditional employer-sponsored routes.

However, this opportunity comes at a significant cost. With a minimum contribution starting at $1 million, the programme is accessible only to a small elite, raising broader concerns about fairness and inclusivity in global migration systems, a Dubai-based immigration specialist told Insider18.

Rayad Kamal Ayub, Managing Director of UAE-based Rayad Group’s Immigration Company, explained that the Trump Gold Card provides a pathway similar to a US Green Card through substantial financial contributions to the US Department of Commerce. The initiative targets individuals with exceptional or extraordinary abilities, as well as professionals whose work serves US national interests, under the EB-1 and EB-2 National Interest Waiver (NIW) visa categories.

In simple terms, the programme allows wealthy foreign nationals to fast-track permission to live in the United States. The launch of an official application form, dedicated website, and filing address has further fueled attention, suggesting that the initiative is actively moving forward.

Despite this momentum, legal experts urge caution. Shai Zamanian, Dubai-based US attorney and Legal Director at The American Legal Centre, told Insider18 that important legal and operational uncertainties remain—particularly when comparing the Gold Card to the long-established EB-5 Immigrant Investor Programme.

One key concern, Zamanian noted, is that the Gold Card was introduced through an executive order, rather than legislation passed by Congress. Unlike the EB-5 programme, it does not rest on a comprehensive legal framework or detailed regulations. As a result, it could face legal challenges in federal court, be altered significantly, or even be cancelled by a future administration without congressional approval. In contrast, EB-5 is firmly embedded in US immigration law, offering investors greater long-term stability and predictability.

Processing speed is another factor investors must evaluate carefully. Zamanian emphasized that faster processing alone does not guarantee quicker residency, as visa availability plays a crucial role. Gold Card applications are expected to draw from EB-1 and EB-2 visa quotas, both of which are already heavily oversubscribed.

Applicants from China and India are likely to be most affected. EB-2 applicants from China already face multi-year delays, while Indian applicants may wait decades. Even EB-1 visas—typically considered faster—are currently backlogged for both countries and could experience further delays as Gold Card demand increases.

By comparison, EB-5 investments in Rural or High Unemployment (Targeted Employment Area) projects remain current for all nationalities. While EB-5 may involve longer adjudication timelines, it currently offers a more reliable and predictable immigration option for many investors, Zamanian concluded.

EB-5 vs Gold Card: Key takeaways

When comparing the EB-5 Immigrant Investor Programme with the Trump Gold Card, several key distinctions stand out.

Under the EB-5 programme, a single qualifying investment covers the primary applicant as well as their spouse and unmarried children under the age of 21. In contrast, the Gold Card model may require each family member to make an individual $1 million contribution to the US government—dramatically increasing the overall cost for families. According to Zamanian, official clarification on how dependents will be treated under the Gold Card framework is still lacking.

Another unresolved issue involves adjustment of status. Zamanian noted that wording in the Gold Card application suggests applicants may be restricted to consular processing only, meaning they would need to remain outside the US while their case is pending. This could limit their ability to live, work, or travel freely during the process. EB-5 applicants, by comparison, are explicitly allowed to submit adjustment of status applications concurrently when eligible, offering far greater flexibility.

Cost structure and financial risk also differ sharply between the two options. The EB-5 programme requires an $800,000 investment in a qualifying project. While the funds are at risk, there is potential for a return, and the investment includes the entire immediate family. Additionally, there is currently no visa backlog for EB-5 projects located in Targeted Employment Areas (TEAs), and the programme operates under clearly defined US immigration statutes.

The Trump Gold Card, on the other hand, requires a $1 million non-refundable contribution per applicant, offers no financial return, and is likely to face visa backlogs. More importantly, it lacks a statutory or regulatory foundation, as it exists solely through executive action.

Zamanian emphasized that although the Gold Card may appeal to certain ultra-wealthy individuals, it carries higher financial exposure, legal ambiguity, and potential delays, especially for families and applicants from countries with existing visa backlogs.

In contrast, EB-5 remains the most established and reliable investment-based route to US permanent residency. Zamanian suggested that prospective applicants may be better served by observing how early Gold Card cases are handled before committing. “Why take unnecessary risks,” he implied, “when EB-5 has been part of US immigration law for nearly 35 years and has consistently enabled families from across the globe to secure lawful access to the United States?

Cost of residing in the US

According to Ayub, the cost of qualifying for the programme is intentionally set at a very high threshold.

For individual applicants, the requirements include a non-refundable contribution of $1 million per applicant, which also applies separately to each dependent, such as a spouse or children. In addition, every applicant must pay a $15,000 filing fee to USCIS. As a result, a household of four would be required to contribute $4 million, along with $60,000 in application fees.

For corporate-backed applicants, the financial commitment is higher. A sponsoring company must make a $2 million contribution for the primary beneficiary, plus $1 million for each accompanying family member. The $15,000 USCIS processing fee still applies to every individual included in the application.

Ayub explained that applicants must provide complete and verifiable records tracing the origin, accumulation, and transfer of funds. The US Department of Commerce first reviews the legitimacy and source of the contribution before USCIS evaluates the immigration application. Only after this approval process are applicants instructed to transfer the funds to a designated US Treasury account. He noted that this rigorous screening process is designed to build public trust and ensure that only credible, financially qualified applicants are approved.

Speaking to Insider18, Ayub said the so-called Trump Gold Card visa marks a significant shift in US immigration strategy. By linking permanent residency to large, transparent financial contributions, the programme aims to attract global investors and entrepreneurs while delivering immediate, measurable economic benefits. For wealthy individuals and business innovators, he added, the initiative provides a clearly defined and regulated route to invest in—and become part of—the US economy.